401(k) Fees: How They Hurt Retirement, Minneapolis, MN

-fees-could-be-eating-away-at-your-retirement.avif)

That 401(k) you’ve been counting on for retirement might just have an unwanted feature: excessive fees. Often 401(k) plan participants are unaware of fees that could be eating away their savings and potentially forcing them to retire later than they want. Not all 401(k)’s are created equal and depending on the plan, these fees could be in excess of $100,000.

If you didn’t know about fees in your 401(k), you’re not alone. Back in 2011, a study by AARP showed that over 70% of 401(k) participants said they did not pay any fees at all. How have so many people been misguided to this fact? The 401(k) was adopted in 1978 and for nearly 30 years, plan providers of 401(k)s did not disclose fees to participants. In 2012 the department of justice ordered 401(k) providers to disclose all fees in participant’s 401(k)s. This is a great step forward, however the fees are often embedded in fund prospectuses and behind many pages of complicated legal jargon.

So, what are these 401(k) fees?

401(k) fees can be divided into two categories:

401(k) plan fees – The list of 401(k) plan fees usually includes record keeping services, trustee and custodial services, and third party administration services. This portion of the fee is usually charged directly as a percentage of your total assets and often is around 0.25-0.4%. These expenses account for the costs associated with running the 401(k), gathering statements and performing the record keeping for each participant.

Investment management fees – This is the largest expense you pay for, and in some cases it is the portion you have the most control over. Each fund you invest in has its own expense ratio, and each fund type varies in its expense level. You can find out your fund’s expense ratio by using the FINRA fund analyzer.

Typically active managed funds have a higher expense ratio compared to passive funds. Actively managed funds hire a fund manager to buy and sell investments to beat a given benchmark yield. The fund manager requires a large salary, and because of their investment activity, could cause trade and tax costs to increase the annual expense ratio. Passive funds track a market weighted index and don’t have a fund manager incurring costs from active trading. This results in lower trade fees, lower taxable events, and much lower fees for you.

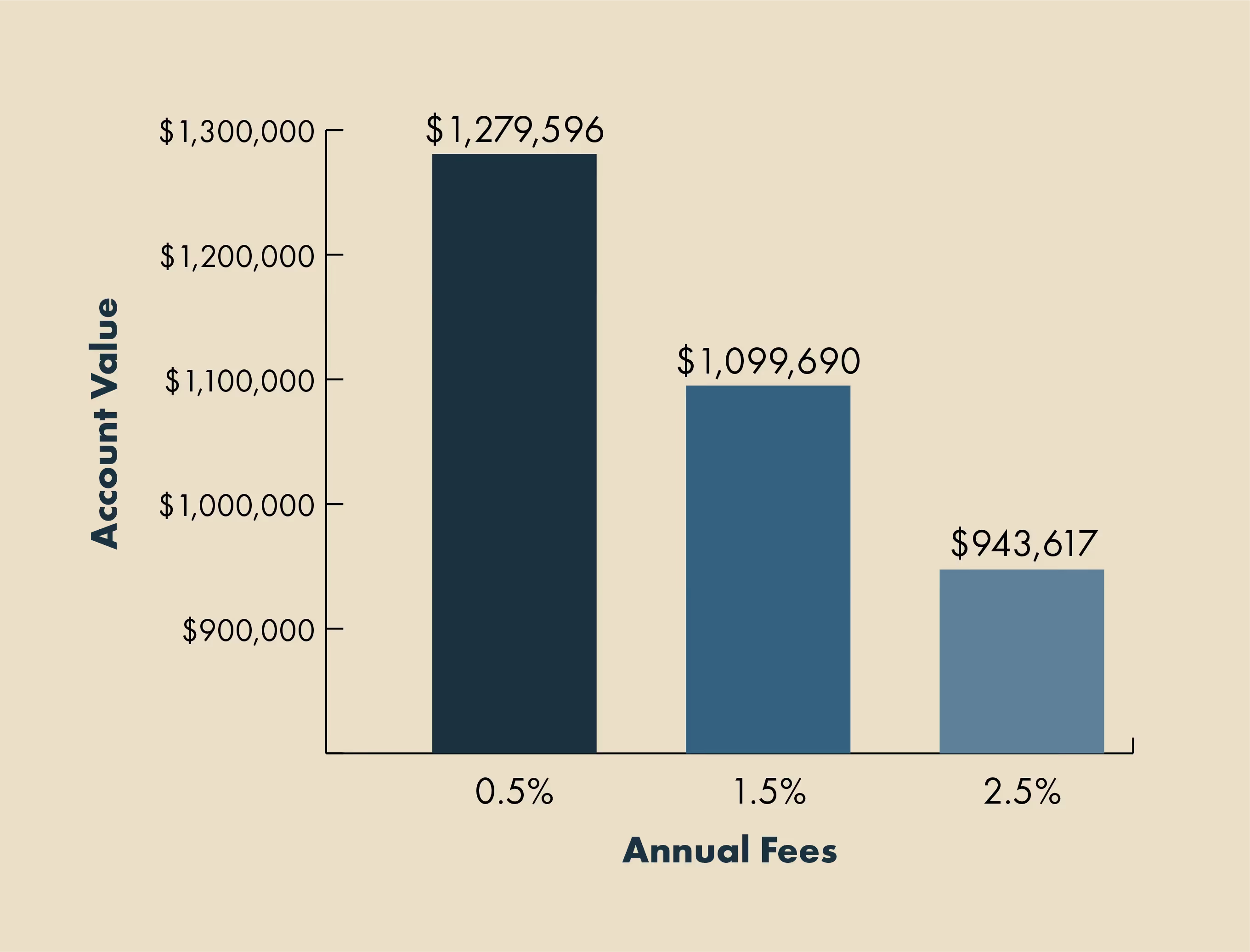

These expenses usually add up to an average of 1%, however depending on your plan and investment choices they can range from 0.5-2.5%. This might not seem like a lot, however with compounding interest, small percentages over time add up quickly.

The chart below shows the impact of fees in a 401k with a beginning account balance of $500,000 over 15 years and compounding 7% annual returns.

A 1% increase in fees from 0.5-1.5% would mean you lose nearly $200,000 in account value.

What can you do about 401(k) fees?

If you’ve determined your expense ratio is not what you’d like it to be, you do have a few options:

- Run your current holdings through the FINRA fund analyzer to see what your funds expense ratio is. If you are in a high cost active managed fund, compare its performance to a similar index fund or ETF if you have them available to you in your 401(k) plan. If there are none available, talk with your plan administrator about adding some low cost investment options in to your plan.

- Highly scrutinize the value your active managed funds are giving you. You might think that a higher expense fund with a fund manager picking stocks would produce a higher return than an inexpensive index fund, however many studies have shown the opposite is true. Over 70% of all active managed funds have failed to beat the market over 10 year periods. Picking low cost index funds will give you the best value overall.

- If you are in a small company, chances are your 401(k) expense ratio is much higher than in a larger company. If you’re open for a job-change, switching to a larger employer with more plan participants could lower the overall fees.

- If you have a 401k you’ve stopped contributions to because you are either retired or no longer at that employer, consider rolling it into an IRA. You’ll have a lot more investment options to choose from.

Your 401k can be one of your best savings tools for retirement. And it’s up to you to make sure its not eaten away by excessive fees. If you want to have your 401(k) statement scrutinized by a professional for free, get in touch with us.

Continue Learning

Gain more Insights and empower your financial future with our articles and other resources.